Everyone pays for car insurance, but very few people understand what they are paying for. It’s not all about finding the best price. More importantly, it’s about getting the right coverage so that when you’re in an accident, you’re covered.

We’ll give you a breakdown of each car insurance coverage. We’ll tell you what the coverage is, why you need it and what level of coverage we recommend.

By the end of this article, you’ll be a car insurance expert!

Remember, each policy and each state is different. So for specific questions, talk to your insurance broker or insurance company.

Table of Contents

Liability Coverage On Car Insurance

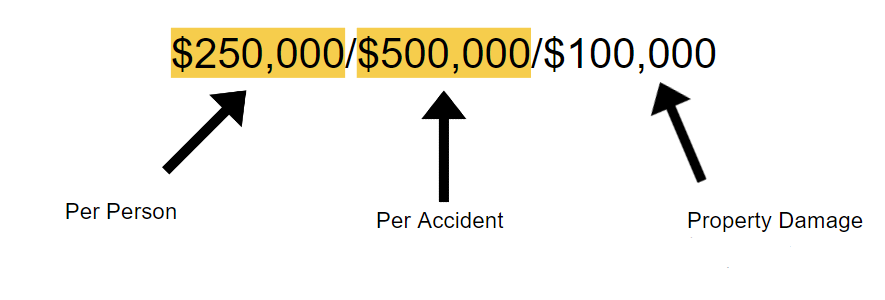

The first coverage that we are going to talk about here is bodily injury liability or bodily injury coverage. This coverage consists of these two highlighted coverages here.

This pays for medical injuries to other people, not yourself. This is not a coverage for you, but this pays for injuries to other people for which you were responsible.

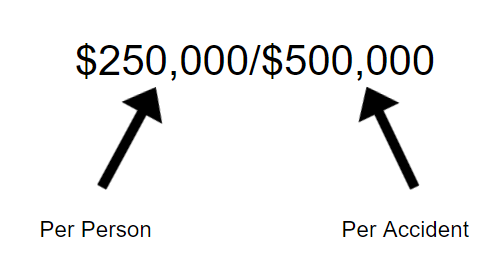

You get to elect the type of coverage that you have here in most states, the minimum is $25,000 per person, $50,000 per accident, which is hardly anything. It goes up from $25,000/$50,000 to $50,000/$100,000 to $100,00/$300,000 to $250,000/$500,000 like we have above.

Example:

Let’s say you are driving down the road. You get a text message, you look at it real quick.

By the time you look back up at the road you slam into the back of a mom who has her one kid in the vehicle and you cause medical injuries to this person. If you have limits of $250,000/$500,000 like we see here your policy would pay $250,000 per person that was in that vehicle for their medical injuries up to $500,000 in total per accident.

What do we recommend?

We recommend you get at least $250,000/$500,000 with a $1 million umbrella. We have other videos & blog posts that talk about umbrella coverage. Check those out here.

Why do we recommend this high of coverage though? You may say “I just want state minimum. I don’t own a house. There’s nothing you can sue me for this and that.”

Well there’s always something that you can be sued for and that’s your income, your job. You get a paycheck every every month or every two weeks. You can always be sued for that. In the example we just gave, where you slam into the back of somebody and you hurt the mom and her child. In today’s day and age, medical injuries can cost a lot of money.

Let’s say that both of those people have to be air evacuated to the hospital. Let’s say each of them needs to have a surgery or two. Let’s say each of them stays in the hospital for a week or two. That $250,000 per person is going to be reached very quickly, that $500,000 per accident is going to be exhausted pretty quickly. And so that’s why we recommend going as high as $250,000/$500,000 with a million dollar umbrella.

You just need to fully protect yourself so that you never have to worry. Even if you don’t have that many assets, you never want to worry about being sued.

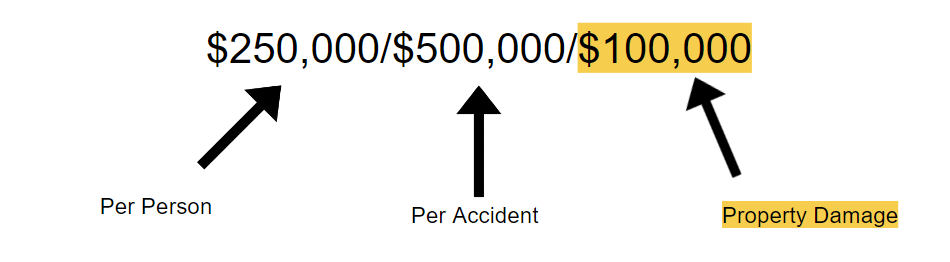

Property Damage Coverage

Property damage coverage pays for property damage of which you were responsible for, again, an at fault accident.

Let’s take our exact same example: You look down at your phone, you slam into the back of somebody you caused the medical injuries which this first part pays for, but you also damage their vehicle and you slam their vehicle into a brick wall on the side of the road.

That’s property damage that you are responsible for. That’s where this coverage kicks in. If you have the limit of 100,000, you have up to $100,000 to pay for the damage to the vehicle and to the damage to the block wall. This can be for anything, if you run into a building, if you run into a light pole, whatever you run into and cause property damage, that’s what this coverage takes care of.

Our recommendation is at least $100,000.

We say that because a lot of times that’s the highest that most insurance companies will go up to. If you can go higher than that do it because it’s not gonna cost you that much money. For instance, I see a lot of policies that have property damage coverage of only $50,000 and then once you bump it up to $100,000, it literally adds like $20 for the whole year, not even per month, but for the whole year, sometimes it’s even less than that.

So you can jack this coverage up pretty high for a very small amount of premium and then you never have to worry about running out of property damage coverage.

Uninsured & Underinsured Car Insurance Coverage

Now we come into a coverage that helps cover you. Let’s use an example and let’s just flip the roles. Let’s say you are at a stoplight and somebody slams into the back of you and causes you medical injuries or your passenger’s medical injuries. This coverage can help pay if that person that slammed into the back of you did not have any insurance coverage or they did not have enough insurance coverage.

So let’s say the person that slammed into you did not have any coverage. You have medical injuries, you have to go to the hospital. His policy obviously is not going to pay for it because he doesn’t have one. So that’s where your policy kicks in, if you have this coverage and helps pay for your medical injuries.

There are other states that offer uninsured property damage coverage. If they do offer it in your state you should purchase it because it’s gonna cost you next to nothing and then if you ever have your car or vehicle damaged by somebody that is uninsured or underinsured, you’re gonna have that coverage. Unfortunately in states like Arizona, it’s not even an option.

So again, this pays for you and your passengers, $250,000 per person up to $500,000 per accident (should you elect those limits). In our agency, we will not sell you a policy that does not have this. We do not want you to reject this coverage and say you don’t want it, it is extremely valuable, especially considering it costs next to nothing to add on to your policy.

There are way too many uninsured and underinsured drivers out there on the road, chances of you being hit by them are growing every day. So just protect yourself and purchase this coverage, we again recommend you purchase $250/500 with a $1 million dollar umbrella.

Now something to point out and if you watch our other videos on umbrella coverage, you will notice and understand that it does not come automatically with uninsured/underinsured.

If you purchase an umbrella policy, it will not come automatic with uninsured underinsured coverage. You have to elect that and specifically tell the insurance company that you want that coverage on your umbrella policy. Make sure you do that.

Very important coverage.

Medical Payments Coverage

Let’s move on to another coverage that is for you, not other people that you hit. This is for you and your passengers should you be in an accident. The cool thing about this coverage is, it is regardless of who is at fault. So whether you were hit or whether you hit somebody else, if you have medical injuries and you have medical coverage, it will help pay for your medical injuries.

You can select coverage options usually $5,000, $10,000 and $20,000. Some companies let you go higher, not a lot of them do. You can choose what you think you need based off of your health insurance and the coverage you have there, you can choose and make your own decision as to high how high of limits you want.

We recommend you get at least $5000 in coverage. It’s so helpful to have that, especially if you’re in an accident that you are at fault. Remember liability does not pay for your medical injuries. So if you don’t have very good health insurance coverage or if you have a high health insurance deductible, you probably want to get at least $5,000 in medical payments coverage.

Again this goes to help pay for your you or your passenger’s medical injuries in an accident regardless of who is at fault.

Collision Coverage On Car Insurance

Now let’s move on to talk more about your vehicle. Up until this point, there has been no coverage for your vehicle.

The first coverage here is collision coverage. This protects your vehicle if it’s been damaged in an accident due to a collision. In other words, for the most part, when we talk about collision, it’s covering your vehicle if it was damaged while your vehicle was moving down the road, so if your vehicle runs into another vehicle, runs into a building, runs into a light pole, things to that nature.

Or if you’re driving down the road and somebody else hits your vehicle, that’s what collision coverage covers. Collision coverage comes in different deductible options from zero all the way up to $2,000.

What does this mean? So let’s say you have a vehicle and it’s damaged and it’s covered under collision and there’s $10,000 worth of damage. Let’s say to make it easy, you have $1000 deductible.

The insurance company is going to pay you the $10,000 of damage minus your $1000 deductible. So you are going to get a $9000 check from the insurance company to go repair your vehicle that has $10,000 worth of damage. You will be responsible for the $1,000 deductible, you will pay that directly to the person or shop that is fixing your vehicle.

It’s not something that you have to pay to the insurance company. You pay it to the person or body shop or a company who is fixing your vehicle.

So what deductible do we recommend you get? Well that again is up to you and your specific situation. We say go as high of a deductible as you can afford.

Why do we say that? The higher the deductible, the lower your monthly insurance premium is going to be. Also, we do not encourage people to file small claims because for every claim you file, it is going to negatively affect your insurance premium. In other words, it’s gonna make your insurance more expensive if you’re filing small, insignificant claims. So we only want to file claims that are worthwhile.

So if you can afford to have a $2,000 deductible you have that in the bank, you should get a $2,000 deductible because your insurance premium is going to be a lot cheaper because you have a higher deductible. So go as high as you can and get that premium as low as you can.

Comprehensive Coverage On Car Insurance

Now the next coverage here is comprehensive coverage. This is a coverage that covers you for everything else that was not covered under collision. Again, a general way to think about it is, this covers you while your car is not moving. For the most part, there are some different examples, there are some caveats, but for the most part while your car is not moving like if it’s vandalized, if it’s stolen, a fire, things to that nature.

The deductible works the same exact way as it does under collision coverage and again we say go as high as you can afford and get that monthly premium as cheap and low as possible.

Full Coverage Car Insurance

Now let’s talk about full coverage. A lot of times people refer to comprehensive and collision as full coverage. We do not like to do that. We like to refer to them as individual coverages and that is because every person and every insurance agent and every insurance company has a different definition of what they think full coverage means.

Some people think that means just adding comp & collision. Some people think it means comprehensive and collision with the $0 deductible including towing and rental. So everybody has a different definition, but for the most part, when someone says I have full coverage, they mean they have comprehensive and collision.

I would encourage you not to use that language because you want to address every coverage individually and specifically so that you know exactly what it is you’re covered for.

Towing Or Roadside Assistance

So this helps you if your vehicle becomes stranded or stuck on the side of the road because you need a tow, you need gas, you have a flat tire, things to that nature.

If you have towing and roadside assistance, your insurance company will come out and help you. Now every company is so much different in terms of what they cover. Like how far they’ll tow you, where they’ll tow you to, if they’ll give you gas if they’ll come out and do the work to give you a spare tire, things to that nature, it’s all different and varies by company.

So you need to check with your specific insurance company to figure out exactly what it is they cover. Now our recommendation, you can see down here might be a little weird but we say if you are really concerned about having good roadside coverage and good towing coverage, buy AAA. It’s a lot more comprehensive of a policy than I’ve seen anywhere else.

Rental Car Reimbursement on Car Insurance

Now let’s move on to our last coverage, rental reimbursement. This helps cover the cost of a rental car should your normal vehicle be in the shop getting fixed due to a covered accident.

The term “covered accident” is important to discuss here. You cannot simply just get a rental car and have the insurance company pay for it because you have a mechanical breakdown or because you want to take a rental car up north for the weekend and you don’t want to drive your own vehicle.

No, this coverage only pays for you to have a rental car if your vehicle is in an accident and it’s a covered accident that your insurance company is paying for it. So if it’s a collision accident or a comprehensive accident and your your car’s in the shop getting fixed, that’s when this kicks in and gives you coverage.

There’s different coverage options available. You can purchase $30 a day, $40 a day or $50 a day up to a 30 day max.

Let’s explain this a little more. Let’s say you select the 50 a day option, your vehicle’s in a covered accident and it’s going to be in the shop for 15 days.

Your insurance company will pay $50 a day for a rental car, which will give you pretty much any car you need or want.

If you’re trying to figure out how much coverage you need. If you should do $30, $40 or $50, think about the car you drive and how often you drive.

If you don’t drive often and you don’t have a super expensive car and you just need to get from point a to point b and you don’t care which vehicle you have, you can go with a lower option of $30 a day. Now if you drive a lot, let’s say you’re a parent that has three or four kids and they have carpool, you’re running them around all day to different activities and you need to make sure that you can fit all of your kids in the vehicle. You need to go up to $50 a day. So that way you can go and get as big of a vehicle as possible so that you can continue to do your normal day to day activities. So we can’t tell you for certain what you should do here. This just depends on your specific situation.

This gives you a good overview so that you know where to start. However, you need to talk to your own agent, your own insurance company to make sure you understand exactly what’s covered on your policy.